CONTINUOUS LEARNING. INDUSTRY ENGAGEMENT.

Credit Union Deposit Insurance Policy - 2/2 - Costs, Benefits & Regulation

There are seemingly three policy options for deposit insurance for B.C. credit unions - Maintain unlimited coverage, Reintroduce limited coverage, Seek provincial alignment. There does not appear a right or wrong policy. But there are policy choices and resultant implications for the B.C. credit union system.

“There are seemingly three policy options for deposit insurance for B.C. credit unions - Maintain unlimited coverage, Reintroduce limited coverage, Seek provincial alignment. There does not appear a right or wrong policy. But there are policy choices and resultant implications for the B.C. credit union system.”

SERIES OVERVIEW

This article is the second part of a two-part series related to deposit insurance applicable to Canadian credit unions.

Overview, History & Pros/Cons: Policy in B.C. & Canada. Unlimited vs limited

Implications & Options: Benefits, cost & regulatory impact. Three policy choices

This series was substantially authored to aid an executive search process. Several system veterans kindly volunteered technical expertise, system memory, and professional guidance. Thank you. Their wisdom, perspective and encouragement were invaluable.

The first article introduced deposit insurance; outlined policy in multiple jurisdictions; and summarized generic pros/cons of limited vs unlimited deposit insurance policies.

This second article has two broad components. First, the implications of unlimited deposit insurance in terms of benefits, costs and regulation. Second, three discrete policy options and recent public positions of the B.C. credit union system. Given subject matter complexity, subjectivity and sensitivity then the author has leveraged significant graphical analysis in efforts to enhance explanation and to aid assessment. Some presented data is marginally stale but this is not believed to impact key themes.

This publication may be easier to read in PDF format. Download per http://bit.ly/dep-ins-pdf

IMPLICATIONS: BENEFITS OF UNLIMITED DEPOSIT INSURANCE

The benefits to B.C. credit unions of a regime of unlimited deposit insurance are broad in nature, and may include -

Market confidence - Growth in collective membership size and deposit amounts at B.C. credit unions

Large depositors - Growth in number or magnitude of deposits that exceeded insurance coverage in other jurisdictions

In-province deposits - Retention of deposits of B.C. members by B.C. credit unions

Depositor Eligibility - it permits institutional entities, such as MUSH (municipal, university, schools and hospitals), to make deposits. Such entities may require that a financial institution have unlimited deposit insurance or a credit rating

Policy simplicity - Members may easily apply unlimited deposit insurance to their circumstances

Between 2007 and 2016 then the B.C. credit union system expanded its membership and attracted larger depositors. System membership increased by over 300,000, from 1.6 to 1.9 million. B.C. member deposits increased from C$36 to C$63 billion. The average member deposit increased from C$22,000 to C$32,000. A range of economic, market and external factors are potential drivers but the dates are also concurrent with the introduction of unlimited deposit insurance. It is possible that unlimited coverage provided members with increased confidence to join, and place higher deposit amounts, with B.C. credit unions.

Unlimited deposit insurance may provide a significant competitive advantage. Three Canadian provinces - BC, SK, MB - have credit union membership that represents in excess of 40% of the population. Each of these provinces has a regime of unlimited coverage. In contrast then Ontario credit union membership represents approximately 10% of its population. The modest market share of credit unions in Alberta and Ontario may be due to the likely strong competition from locally headquartered entities of ATB Financial and Canadian banks respectively.

“B.C. member deposits increased from C$36 to C$63 billion. The average member deposit increased from C$22,000 to C$32,000.”

Unlimited deposit insurance may have attracted larger depositors. At December 2015 then four provinces, each with unlimited coverage, have average credit union deposits in excess of C$30,000 while Ontario credit unions report less than C$25,000. Caution is appropriate with statistics. Higher average member deposit could indicate that many members have increased their deposits or suggest that a modest number of members, perhaps non-consumer, have placed outlier large deposits.

Limited data available in regards the retention of B.C. deposits in B.C. credit unions. It may be notable that, at December 2015, over half of the C$4.2 billion deposits at Concentra Financial were from Ontario customers.

IMPLICATIONS: COSTS OF UNLIMITED COVERAGE

Quantifying the cost of unlimited deposit insurance is tricky. Unlike typical insurance products, the buyer cannot seek a quotation from an alternative service provider or consider costs under multiple coverage insurance terms. Quantifying alternative deposit regimes is beyond the remit of this brief article. But comparable metrics of deposit funds may provide insight -

Historical B.C. levels - Fund levels prior to the introduction of unlimited coverage for B.C. credit unions

Other ‘unlimited’ provinces - Fund levels in other Canadian provinces that offer unlimited deposit insurance

‘Limited’ coverage entities - Fund levels applicable to deposit taking institutions subject to limited deposit insurance

Following the introduction of unlimited coverage, the cost of deposit insurance increased materially. Between 2007 and 2016 then B.C. deposit insurance funding increased from 76 to 95 basis points of member deposits at credit unions. Per current insurer targets then funding is expected to reach 118 basis points by 2021. Higher basis point funding can be associated with an insurer perception of elevated expected loss, say from increased claim sizes (exposure at default) or higher probability of claim (probability of default) that may arise from unlimited deposit coverage or challenging economic conditions.

The B.C. policy may be funded to a lesser extent than funds in provinces with similar coverage. Three other Canadian provinces offer unlimited insurance and each has a higher level of fund size, in terms of basis points of than that of B.C. Relative to its peers then annual assessments may rise the greatest in B.C. as it is currently furthest from its target funding levels.

As is typical of insurance, the fund capital is proportional to insurable risk. For deposit taking institutions, such as credit unions, the size of ex-ante fund increases with the magnitude of insurable deposits and so indirectly by deposit insurance policy. Ontario credit unions, federal credit and banks are each subject to C$100,000 deposit insurance. Related deposit insurer funds are, in basis points terms, materially smaller than in any of the provincial funds that provide unlimited insurance.

“Following the introduction of unlimited coverage, the cost of deposit insurance increased materially.”

While the cost of unlimited coverage requires significant analysis, the author suggests a few ballpark frames of reference-

Were 2007 funding (76bp) effective in 2016 then B.C. credit unions may have an estimated C$100 million more capital

Were 2016 ex-ante funding metrics in B.C. consistent with Ontario then the B.C. funds could be smaller by almost C$200 million

The forecasted increase in target fund levels may account for approximately C$15 million of annual CUDIC assessments

Published 2012 target funding may require continuance or escalation of CUDIC assessments at 18% of system earnings

IMPLICATIONS: REGULATION AND DEPOSIT INSURER

The author considers that unlimited deposit insurance for B.C. credit unions includes discrete financial implications:

Large depositors* - Growth in number or magnitude of high-value deposits enables lending but may increase liquidity risk

Annual premiums* - Elevated exposure at default increases insurance assessments to build a larger investment pool

Opportunity cost* - A larger insurance fund dilutes current earnings and reduces capital adequacy of credit unions

Market confidence** - Growth in membership size and deposit amounts at B.C. credit unions

In-province deposits** - Policy competitiveness encourages retention of deposits of B.C. members by B.C. credit unions

Regulatory compliance** - Insurance risk supports regulatory guideline issuance and supervisory expectation intensity

* High probability, ** Medium probability (author assessment)

CUDIC 2016 assessments represented 18% of the net income of the B.C. credit union system. This proportion is up from 14% in 2014. CUDIC assessments appear to wholly increase its investment asset pool. Between 2014 and 2016 then CUDIC investment portfolio returns have exceeded all expenses and taxes. CUDIC expenses include approximately $5 million charged, but significantly unspent, by FICOM. Deposition by Tara Richards, FICOM Acting CEO, to the B.C. Legislative Assembly states that ‘with the shortage of staff, we have a surplus ... of $3.5 million to $5 million on an annual basis. Last year [to 31 March 2015], for the record, the recovery [unspent income returned to B.C. government general fund] was $4.8 million’.

The B.C. ex-ante deposit insurance funds have increased in size relative to the aggregate capital of B.C. credit unions. In 2007 then the asset pools represented 12.2% of system capital but this had increased to 14.6% in 2016. Were the equity of Coast Capital Savings Credit Union excluded, assuming its future achievement of federal charter without CUDIC coverage, then the insurance asset pools would represent almost 20% of system. Payments by B.C. credit unions to CUDIC reduce their net income and, over time, retained earnings and capital adequacy.

In recent years regulatory compliance costs of B.C. credit unions may have increased materially. Based on the substance and frequency of regulatory guidance issuance the level of oversight appears to have expanded at an ever greater rate. Between 2013 and 2016 FICOM issued seven Guidelines; required extended reporting on various topics; and executed several system-level initiatives, such as stress tests. Some Guidelines issued by FICOM have resulted from task force or other consultative processes that involved executives, board members or advisors from B.C. credit unions.

CONCLUSION: POLICY OPTIONS

Option 1 - Maintain current unlimited deposit insurance regime

The current regime may have supported growth, reinforced strength and showcased confidence within the B.C. credit union system. During the current regime period then membership size and deposit amounts collectively at B.C. credit unions have increased by 19% and 72% respectively. Unlimited insurance appears to have attracted larger depositors, with average member deposits increased by 45%. System capital has increased by 78%. All Western Canadian provinces offer unlimited coverage.

The B.C. credit union system and most individual credit unions to be materially supportive of the current regime.

But an elevated level of moral hazard may enable inappropriate risk appetite, insufficient risk management or unsound business practices by B.C. credit unions. The regime is increasingly expensive. Assessments drain 18% of credit union system earnings. The ex-ante funds represent almost 15% of system capital. Regulatory requirements have intensified and compliance costs increased. Unlimited insurance may be acutely costly for credit unions under regulatory intervention.

Option 2 - Reintroduce a limited deposit insurance regime

Many depositors may want rather than need unlimited deposit insurance. Deposit taking institutions with limited deposit insurance have significant levels of uninsured deposits. 30% of deposits in Ontario credit unions are uninsured by DICO. 72% of deposits in banks and federal credit unions are uninsured by CDIC. Yet DICO and CDIC regimes currently apply maximum coverage of C$100,000 per depositor per account type. Per its federal credit union disclosures, fewer than 4% of personal members of Coast Capital Savings Credit Union have deposits that exceed CDIC's limited policy coverage.

The author understands that the current deposit insurance regime was introduced by the B.C. government as a surprise to, rather than at the request of, the B.C. credit union system. The re-introduction of limited deposit insurance could boost credit union earnings, redeploy system capital, simplify consumer expectations and/or ease regulatory burden. This may be welcomed given significant financial margins compression; elevated member expectations and technology investment; the system FIA/CUIA submission theme of ‘every bit of capital counts’; and 2014 and 2016 Auditor General of B.C. findings of resource challenges at the provincial regulator. Credit unions may ensure their adoption of sound risk management practices.

But limited coverage could negatively impact B.C. credit unions. Members with large deposit balances, market confidence sensitivities or depositor profile requirements may migrate their deposits outside of B.C. credit unions. The potential impacts of any material withdrawals from the B.C. credit union system include lending capacity, liquidity position, earnings potential and/or economic growth. Any regime transition need be carefully implemented and thoughtfully communicated to both B.C. credit unions and to their membership.

Option 3 - Seek alignment of deposit insurance regimes across provincial jurisdictions

Few, if any, significant jurisdictions outside Western Canada have deposit insurance regimes that provide unlimited coverage. Some jurisdictions introduced unlimited coverage regimes to consciously have a temporary impact. Credit unions in Ontario, Quebec and Atlantic Canada; all Canadian banks and federal credit unions; and most, if not all, deposit taking institutions in Europe and U.S.A. operate in deposit insurance regime with limited coverage. Federal credit unions will likely gain traction.

There may be an opportunity to concurrently align deposit insurance regimes in Canada. Any use of a deposit insurance regime to attract out-of-province deposits may be contrary to the principle of ‘cooperation among cooperatives’, may encourage in a race-to-the-bottom policy mindset, and/or may concentrate risk within provincial systems with the highest risk appetite. A regime could potentially distinguish between insurance coverage for members that reside in-province versus out-of-province.

But such changes would likely be complex, political and lengthy. Related regimes are enacted in provincial policy design and legislative execution would require buy-in from multiple provincial governments and demand extensive system resource. Some provincial credit union systems may be significantly adverse to the policy concept. A consistent regime between both credit unions and banks is likely infeasible, partly as large Canadian banks are effectively too-big-to-fail.

CONCLUSION: B.C. CREDIT UNION SYSTEM VIEW

Submissions to the B.C. Ministry of Finance FIA/CUIA review provide insight into the related views of B.C. credit unions.

Individual credit unions

The B.C. Ministry of Finance website in regards the FIA/CUIA Consultation process provides weblinks to submissions by ten individual credit unions. This represents approximately one-quarter of the number of B.C. credit unions, and likely a significantly higher proportion of its membership and deposits.

“Input Received from Stakeholders’ document notes that “Overall, most individual credit unions making submissions expressed strong support for retaining unlimited deposit insurance.”

One B.C. credit union, Community Savings Credit Union, provided significant critical commentary and provided details of its historical CUDIC assessments, that increased by 575% between 2008 and 2014. Its submission highlights the ‘subjective assessment by FICOM’ and the 2012 CUDIC methodology change as key related drivers, in addition to the typical impact of increased aggregate member deposit balances.

B.C. credit union system

The credit union system submission reiterates its prior stance in support of a regime of unlimited deposit insurance.

‘The system is thus still united in its position from the last substantive legislative review where it argued “as integral components of their communities and their regional economies, credit unions have played a ... role in providing financial services to public bodies. Each of these public bodies is responsible for raising and administering public monies.'

Further, the system response makes an express recommendation that 'the deposit insurance regime must respect the following five principles:

Maintenance of a competitive credit union system;

Supports provincial money staying in the province;

Recognizes the value of self-regulation in the system;

Is easily understandable by depositors; and

Any transitions must be well thought out and very carefully managed.'

“[B.C.] credit unions had unlimited deposit insurance between 1968-1988 with no evidence of problems.”

CONCLUSION: RECOMMENDATIONS

The author suggests that deposit insurance policy is neither a question of right or wrong, nor of decisions on isolated topics. But rather of choices and their collective implications to all stakeholders. Would B.C. credit unions be more inclined to advocate for limited deposit insurance if it were accompanied by lower CUDIC assessments, rebated CUDIC capital, aligned jurisdictional policies and/or lesser regulatory intensity?

This report is intended as a discussion document. The author expresses no opinion and proposes no recommendation.

This concludes the second article of a two-part series. For reasons of brevity, this report does not significantly consider related implications of current and emergent federal credit unions; the legislative history in jurisdictions other than B.C.; the mandate fulfilment by B.C. deposit insurer(s); the value-for-money of relevant services; or the funding levels, roles and responsibilities, or other matters between CUDIC and SCCU.

REFERENCES

B.C. Deposit Insurance Organizations

CUDIC: Guide to BC Credit Union Deposit Insurance - http://www.cudicbc.ca/pdf/cudic/CUDICGuide.pdf

CUDIC: Target Fund Policy - http://www.cudicbc.ca/pdf/cudic/TargetPolicy.pdf

CUDIC: 2016 Annual Report - http://www.cudicbc.ca/pdf/cudic/CUDICFinancials2016.pdf

Stabilization Central: Annual Reports - https://www.stabil.com/about/

Other Selected Deposit Insurance Organizations

CUDGC (AB) - http://www.cudgc.ab.ca

CUDGC (SK) - https://www.cudgc.sk.ca/about-us/

DGCM (MB) - http://depositguarantee.mb.ca/home/

DICO (ON) - http://www.dico.com/design/0_0_Eng.html

CDIC - https://www.cdic.ca

NCUA - https://www.ncua.gov

B.C. Ministry of Finance

FIA/CUIA Consultations - http://www.fin.gov.bc.ca/pld/fiareview.htm

FIA/CUIA Consultations Stakeholder Summary - http://www.fin.gov.bc.ca/pld/files/Response%20report%20to%20FIA%20review%20initial%20consultation%20paper.pdf

FIA/CUIA System Response - http://www.fin.gov.bc.ca/pld/files/BC%20Credit%20Union%20System%20Response.pdf

FIA/CUIA Response of Community Savings Credit Union - http://www.fin.gov.bc.ca/pld/files/Community%20Savings%20Credit%20Union%20(CSCU).pdf

BC Select Standing Committee on Public Accounts - Draft minutes, October 2016 - https://www.leg.bc.ca/documents-data/committees-transcripts/20161005am-PublicAccounts-Vancouver-Blues

Other References

Coast Capital Savings CU: CUDIC vs CDIC deposit insurance coverage - Report: https://www.coastcapitalsavings.com/SharedContent/documents/OnlineVoting/2016/ContinuanceBooklet.pdf

C.D. Howe Institute, ‘A New (Old) Way of Thinking about Financial Regulation’ (2014) - Report: https://www.cdhowe.org/sites/default/files/attachments/research_papers/mixed/Commentary_401_0.pdf

FDIC: Termination of unlimited deposit insurance - https://www.fdic.gov/news/news/financial/2012/fil12045.html

FSB: Guidance for Developing Effective Deposit Insurance Systems - http://www.fsb.org/wp-content/uploads/r_0109b.pdf

Time: Why ... a Huge Decline in Drivers Licenses - http://time.com/money/4185441/millennials-drivers-licenses-gen-x/

OECD: ‘Financial Turbulence - Some Lessons Regarding Deposit Insurance’ (2008) - Report: http://www.oecd.org/pensions/insurance/41420525.pdf

CATO: ‘The Explicit Cost of Government Deposit Insurance’ (2014) - Report: https://object.cato.org/sites/cato.org/files/serials/files/cato-journal/2014/2/v34n1-8.pdf

FDIC: ‘Deposit Insurance Reform: State of Debate’ (1999) - Report: https://www.fdic.gov/bank/analytical/banking/1999dec/1_v12n3.pdf

CCUA: 2015 Annual Report - https://www.ccua.com/~/media/CCUA/member_corner/publications/pdfs/CanadianCentral_AnnualReport_2015.pdf

World Bank: ‘Deposit Insurance Around The World - Issues of Design and Implementation’ (2008) - Report: https://mitpress.mit.edu/sites/default/files/titles/content/9780262042543_sch_0001.pdf

NBER: ‘Deposit Insurance Around the Globe’ (2001) - Report: http://www.nber.org/papers/w8493.pdf

Book: ‘Stress Tests: Reflections on Financial Crises’ (2014) - Book: https://www.amazon.ca/Stress-Test-Reflections-Financial-Crises/dp/0804138591

ACKNOWLEDGEMENT

The author wishes to thank selected credit union system veterans that generously volunteered technical expertise, system memory and professional guidance. Out of discretion then no names are noted. Thank you. Their wisdom, perspective and encouragement were most appreciated.

DISCLAIMER & COPYRIGHT

This article reflects the personal comments of the author, Ross McDonald. This article does not represent the views of any financial cooperative, corporate organization, regulatory body or government ministry. Comments are wholly based on information that is in the public domain.

Although the author has made every effort to ensure that the information in this article was correct at press time, the author does not assume and hereby disclaim any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

All rights reserved.

Credit Union Deposit Insurance Policy - 1/2 - Overview, History, Pros & Cons

A policy of unlimited deposit insurance may have significantly supported system growth and membership confidence. But it is unknown outside of Western Canada, may cause moral hazard, and may be increasingly expensive to credit unions in terms of earnings, capital and compliance.

“A policy of unlimited deposit insurance may have significantly supported system growth and membership confidence. But it is unknown outside of Western Canada, may cause moral hazard, and may be increasingly expensive to credit unions in terms of earnings, capital and compliance.”

SERIES OVERVIEW

This article is the first part of a two-part series related to deposit insurance applicable to Canadian credit unions.

Overview, History & Pros/Cons: Policy in B.C. & Canada. Unlimited vs limited

Implications & Options: Benefits, cost & regulatory impact. Three policy choices

This series was authored earlier in 2017 to aid an executive search process. A formatted PDF of the article series is available on request and will be published in due course. Several system veterans kindly volunteered technical expertise, system memory, and professional guidance. Thank you. Their wisdom, perspective and encouragement were invaluable.

This article has five sections - Executive summary; Deposit insurance; Canadian provincial credit unions; B.C. credit unions; Unlimited vs limited coverage.

Given subject matter complexity, subjectivity and sensitivity then the author has leveraged significant graphical analysis in efforts to enhance explanation and to aid assessment.

This document may be easier to read in PDF format. Download per http://bit.ly/dep-ins-pdf

EXECUTIVE SUMMARY

“Deposit insurance policy may gain prominence due to emergent federal credit unions and a current B.C. legislative review.”

Most credit unions, banks and other deposit taking institutions are legally obligated to maintain deposit insurance. Such insurance refunds depositors in the event of institutional insolvency. An ‘ex-ante’ policy involves the establishment of a fund to subsequently settle claims. Canada has multiple deposit insurers that collectively manage approximately C$5 billion of investment funds. Deposits in B.C. credit unions are covered by Credit Union Deposit Insurance Corporation (CUDIC) and by Stabilization Central Credit Union (SCCU) that collectively manage approximately C$600 million of investment funds.

The coverage terms and resultant cost of deposit insurance vary materially across Canadian deposit taking institutions. Deposi- tors in some institutions, including B.C. credit unions, currently receive insurance to an unlimited amount.

Individual credit unions can mitigate assessment cost through prudent operations, regulatory compliance and good gover- nance. Collectively, credit unions may influence deposit insurance by policy advocacy for coverage terms and target funds.

For some credit union industry stakeholders, deposit insurance policy is an acutely sensitive topic. Elevated, or unlimited, levels of deposit insurance coverage is a competitive advantage for some credit unions against Canadian banks. Over recent decades then B.C. credit unions have operated in regimes that offer both unlimited and limited coverage. There are advantages and disadvantages, costs and benefits of each policy and there are international best practices.

Deposit insurance policy may gain prominence due to federal credit unions and a current B.C. legislative review.

A hybrid future with federal and provincial credit unions may create four implications for deposit insurance - entity funding, policy inconsistencies, consumer confusion and deposit transition. Provincial ex-ante deposit insurance funds may retain historical premiums paid by federal credit unions, potentially creating material insurance surplus. Deposit insurance policies across Canadian jurisdictions and between entity types currently vary materially and may differ from international practices. There is a risk that consumers may not understand the difference in deposit insurance coverage offered by a federal credit union and a provincial credit union. The transition from a provincial to a federal credit union may displace a subset of deposi- tors, say those with relatively large account balances. This article does not expressly address federal credit union matters.

An active legislative review by the B.C. Ministry of Finance is considering the optimal level of deposit insurance for B.C. credit unions. FIA/CUIA submissions by the B.C. credit union system and by most, but not all, individual credit unions appear to significantly support the maintenance of the current regime of unlimited deposit insurance. Data suggests that this regime may have supported growth in membership, deposits and market share of the B.C. credit unions. Further, the regime may have contributed to the relatively strong market share by, and large average member deposits in, B.C. credit unions compared with provinces that have limited coverage. But a policy of unlimited deposit insurance is unknown outside of Western Canada, may cause moral hazard, and may be increasingly expensive to credit unions in terms of earnings, capital and compliance.

This article seeks to stimulate collaborative discussion. It may highlight history or facts that are unfamiliar. It may aid profes- sional education or support policy formulation by the Board or executive of a credit union or system entity. In this article, most analysis related to B.C. aggregates information for CUDIC and SCCU. The report is framed in the following sections-

Overview: Deposit insurance; Deposit insurance in Canada; Deposit insurance in B.C; Pros & Cons of alternate regimes Implications: Bene ts of unlimited coverage; Costs of unlimited coverage; Regulation & Deposit insurer Conclusions: Policy options; B.C. credit union system view

References, About the author, Disclaimer

As a discussion document, it consciously does not provide a policy recommendation. But it does strive to gather objective data; present relevant analysis; consider advantages, disadvantages, and implications; and frame three discrete policy options.

Maintain current policy of unlimited deposit insurance

Re-introduce policy of limited deposit insurance

Seek policy alignment of deposit insurance across Canadian jurisdictions

DEPOSIT INSURANCE OVERVIEW

Many jurisdictions or legislatures require that their deposit taking institutions maintain deposit insurance. Most North American deposit insurers were established decades ago.

First deposit insurance entity - Reportedly by Czechoslovakia

US banks - US established the Federal Deposit Insurance Corporation (FDIC) following the 1933 banking crisis

Canadian banks - Canada established the Canada Deposit Insurance Corporation (CDIC) in 1967

US credit unions - US National Credit Union Share Insurance Fund (NCUSIF), administered by the National Credit Union Administration (NCUA), was created by Congress in 1970

BC credit unions - Credit Union Deposit Insurance Corporation of British Columbia (CUDIC) was formed in 1958

BC credit unions - Stabilization Central Credit Union (SCCU) was created by legislation in 1989

EU - Member state requirements introduced in 1994 with policies subsequently increased and harmonized

Deposit insurance entities actively manage risk and monitor deposits. Assumptions on risk drive actuarial models that typically frame target fund size. is mitigated through of legislative requirements; issuance of regulatory guidelines; maintenance of prudential supervision and oversight of market conduct. Each function may be operationally executed by the deposit insurer staff or outsourced to a government entity or other entity. Insurers may penalize financial institutions that are perceived as high risk. Assessed premiums may be elevated if a deposit taking institution is subject to active regulatory intervention; reports poor or deteriorating financial performance; or has other factors that suggest elevated depositor risk.

The terms of deposit coverage are determined by legislation and can change over time. Currently, coverage for Canadian institutions varies from C$100,000 to unlimited. European Union members coverage of EUR 100,000. U.K. offers coverage of GBP 85,000. Terms in jurisdictions, including the UK, are significantly more restrictive than in Canada - a UK depositor is insured for GBP 85,000 per financial institution where a Canadian depositor is insured per account type (e.g. C$300,000 across TFSA, RSP and taxable accounts in a jurisdiction with C$100,000 coverage) per financial institution. During the 2008 financial markets challenges the then B.C. government replaced limited with unlimited coverage for member deposits at B.C. credit unions. In 2012 then U.S. authorities consciously let lapse legislation that provided temporary unlimited insurance at FDIC, a major U.S. deposit insurer, thereby resuming coverage up to US$250,000.

Canadian provincial credit unions are mandated members of a provincial deposit insurance fund while banks and federal credit unions are mandated members of Canadian Deposit Insurance Corporation (CDIC). All Canadian deposit insurers are funded on an ex-ante basis. Under this approach then each financial institution member makes regular financial contributions to build a collective fund that is intended to settle the costs of any future claims.

Multiple types of Canadian entities provide deposit insurance. Depending on the applicable legislation then the provider may be a provincial government ministry, a provincial crown corporation, and/or a credit union system organization. Related stakeholder representation, nominations authority and regulatory independence vary.

Critics highlight moral hazard concerns, that escalate commensurately with the level of insurance. Depositors, reliant on full reimbursement, may place minimal effort to select or to monitor their financial institution. Deposit taking institutions may be incentivized to undertake elevated risks, underprice risk, and/or insufficiently adopt sound risk management practices.

DEPOSIT INSURANCE IN CANADIAN PROVINCIAL CREDIT UNIONS

Deposit insurance coverage terms vary materially. The monetary value, depositor profile and account type that are eligible under deposit insurance regimes are markedly different across different provincial credit union systems; between provincial credit unions and federal credit unions; and between provincial credit unions and banks.

Western Canadian provincial governments all currently have legislated regimes that provide unlimited deposit insurance to their provincial credit unions. Depositors in other provincial credit unions are subject to maximum coverage between C$100,000 and C$250,000. Federal credit unions and banks are subject to C$100,000 deposit insurance.

Deposit insurance is impacted by federal charter. Should it secure a federal charter then member deposits of Coast Capital Savings Credit Union would be insured to C$100,000. Coast Capital Savings Credit Union, in its member documentation related to federal credit union resolution, included informative tables that outlined the deposit insurance regimes of CUDIC (provincial credit union) and CDIC (banks and federal credit unions).

Where deposit insurance is capped, limits are usually by account type and may not apply to registered accounts. Depositors may have the ability to arrange their banking affairs across more than account type or deposit holder to achieve higher levels of aggregate deposit insurance.

Deposit insurance amounts typically apply per account type per person per financial institution. A couple residing in a jurisdiction with maximum C$100,000 deposit insurance may be able to access in excess of $500,000 deposit insurance coverage between RSP, TFSA and taxable accounts for each person - or multiple times that level if deposits are spread across multiple financial institutions. Some international jurisdictions have more restrictive policies that aggregate accounts per institution.

Some may question the strategic need for, and perhaps operational of, elevated or unlimited deposit insurance policy for any credit union. Historically, credit unions may have courted the operational banking needs of small community members rather than high net worth or institutional depositors.

All depositors do not appear to require unlimited insurance. At December 2015, 30% of member deposits in Ontario provincial credit unions were uninsured, being in excess of the maximum amount or otherwise ineligible under DICO terms. At March 2016, 73% of deposits with CDIC members were uninsured.

DEPOSIT INSURANCE IN BRITISH COLUMBIA CREDIT UNIONS

B.C. credit unions are required by the Financial Institutions Act to be members of Credit Union Deposit Insurance Corporation (CUDIC) and of Stabilization Central Credit Union (SCCU).

CUDIC is a provincial crown corporation that is administered by the Financial Institutions Commission (FICOM), an agency of the BC provincial government.

SCCU is a cooperative organization that is owned by BC credit unions and managed by a small dedicated team.

Each related entity is wholly governed by nominees of either the government or the credit union system. Currently, the Superintendent and Commission of FICOM are also the CEO and Board of CUDIC, with Commission/Board members appointed by the Lieutenant Governor in Council. While the Board of SCCU is comprised of executives and directors of credit unions, largely appointed by credit union peer groups.

CUDIC and SCCU collectively manage almost C$0.6 billion of investment assets. SCCU currently provides CUDIC with coverage of the first C$30 million of depositor losses. In the event of a deposit claim larger than available CUDIC assets, the B.C. government may - but is not required to - provide incremental funding to CUDIC to settle depositor losses.

The evolution of ex-ante investment assets, roles & responsibilities, and stakeholder relationships between SCCU and CUDIC /FICOM, while of potentially significant historical impact and future opportunity, are beyond the scope of this article.

A system-led deposit insurance fund was introduced in B.C. in 1968 following credit union losses that required financial support from the B.C. credit union system to permit the refund of member deposits. Unlimited coverage, insured by the credit union system, was effective from 1968 to 1988. In 1988 then B.C. government formally legislated an explicit deposit insurance guarantee but imposes a limited regime that was capped at C$100,000. This compared to C$60,000 coverage at Canadian banks. Limited coverage applied until 2008, at which time the BC provincial government replaced the then limited regime with an unlimited regime, partly in response to the then turbulence in financial markets and economic conditions. To the knowledge of the author then, in 2008, the current unlimited deposit insurance regime in B.C. was proposed by the provincial government rather than requested by the credit union system.

Deposit insurance premiums represent a material cost to B.C. credit unions. CUDIC 2016 assessments represented approximately 18% of the net income reported by the B.C. credit union system (C$46.7m and C$260.9 million respectively).

The extent of credit union deposits that would become uninsured the B.C. government to re-introduce a regime of limited deposit insurance is not publicly quantified. But insight is available from Coast Capital Savings Credit Union. In documentation issued to members prior to its federal credit union resolution then Coast Capital Savings disclosed that “As of July 2016, fewer than 4% of Coast Capital Savings’ personal members require deposit insurance beyond $100,000. This means the eligible deposits of 96% of our personal members fall within CDIC’s coverage limits today.” The dollar value of member deposits in excess of C$100,000 may represent a materially larger amount than 4% of total member deposits given that, by definition, noted personal members have relatively large deposits and there may also be ineligible deposits from non-personal members. Further insight may be available from the significant level of non-insured deposits in Ontario credit unions and in Canadian banks, each of which currently has coverage capped at C$100,000.

“A credit union opting to continue into the federal jurisdiction would not be able to bring their funds that were provided to CUDIC to the federal jurisdiction. Those funds would be retained by CUDIC.”

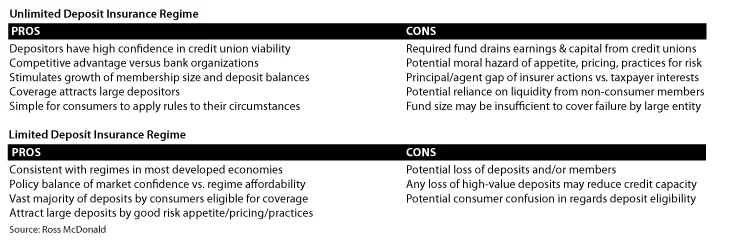

PROS & CONS OF UNLIMITED AND LIMITED DEPOSIT INSURANCE

A significant number of policy and economic papers have been written on deposit insurance regimes and related topics. This may reflect the increased adoption, over recent decades, of deposit insurance regimes internationally. Most, if not all, papers that consider alternative regimes do so between those with limited deposit insurance versus no insurance. The absence of policy critique in regards unlimited coverage may reflect the exceptional rarity of such policies outside of Western Canada.

Deposit insurance can bolster depositor confidence, especially in times of uncertain market or economic conditions. Former US Treasury Secretary Tim Geithner, in his thoughtful book 'Stress Test', may frame such a policy as ‘putting money in the window’ to visibly demonstrate sufficient liquidity and to prevent bank runs - typically on a short-term basis. It may also represent a legislated competitive advantage, to encourage depositors to place savings at institutions with favorable insurance regimes. Regime competition can distort the profile of depositors and borrowers, and/or create treasury dependence on liquidity from non-consumer and/or out-of-market depositors.

Critics of deposit insurance typically frame two conceptual concerns - moral hazard and principal/agent gap. Each of these concerns applies in a limited coverage regime and is likely significantly augmented in a regime with unlimited coverage.

Moral hazard refers to the incentive for insured financial institutions to engage in riskier behavior than would otherwise be feasible. Depositors in insured institutions may conduct limited selection or ongoing monitoring. Executives in insured institutions may set an appetite, risk in products and/or tolerate poor risk management practices. In aggregate then this may cause excessive risk taking, economic resource misallocation, bank failures and/or higher remedial costs. Losses will be absorbed by the institution before deposit regulators may mitigate moral hazard risks through higher capital adequacy requirements; greater prudential supervision intensity; and/or rigorous intervention penalties or processes.

Principal/agent gap refers to potential disconnects between the incentives of the agent (regulator or elected official) and the interests of the principal (taxpayer). The FDIC notes that agents may “ignore the problems of troubled institutions and delay addressing them in order to cover up past mistakes; wait for hoped-for-improvements in the economy; avoid trouble ‘on their watch’ or serve some other purposes of self-interest”. the principal lacks the information or power to effectively monitor the agent. Challenges may delay remedial action and/or institution closure, ultimately increase the cost of a resolution.

This concludes the first article of a two-part series. The second part will present significant objective evidence and supporting commentary to explore related and regulatory implications; and will frame three discrete policy options. A list of sources and references will be appended to the final article in this series.

DISCLAIMER & COPYRIGHT

This article reflects the personal comments of the author, Ross McDonald. This article does not represent the views of any financial cooperative, corporate organization, regulatory body or government ministry. Comments are wholly based on information that is in the public domain.

Although the author has made every effort to ensure that the information in this article was correct at press time, the author does not assume and hereby disclaim any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

All rights reserved.