CONTINUOUS LEARNING. INDUSTRY ENGAGEMENT.

High Quality Liquid Assets (HQLA) - Treasury tactics

Household pets have been covering their ears. During the first calendar quarter, once reticent finance executives, and finance-engaged CEOs, of B.C. and ON credit unions may have been raging expletives. It’s been a frustrating, challenging and unfamiliar period. Financial instruments once wholly alien to small Canadian credit unions, perhaps large ones too, are now commonplace.

‘A turn in the road is not the end of the road, unless you fail to make the turn’ - Anonymous

Household pets have been covering their ears. During the first calendar quarter, once reticent finance executives, and finance-engaged CEOs, of B.C. and ON credit unions may have been raging expletives. It’s been a frustrating, challenging and unfamiliar period. Financial instruments once wholly alien to small Canadian credit unions, perhaps large ones too, are now commonplace. A whole new lexicon of investment terminology has been explored, digested and applied. Stakeholder reporting may have underwhelmed expectations. New journal entries may have being imagined from first principles. Financial reports and risk oversight may require a refresh. BCFSA has a new guideline and a new regulatory report (and several consultations). And your prudential supervisor Relationship Manager has requested a touch-base video conference call, again.

Note: A formatted, graphical PDF version of this article is available at https://www.bitly.com/rm-hqla

Almost two years ago, FICOM issued a decree. The ‘mandatory liquidity pool’ structure was dead. It had been used for decades to execute credit union compliance with Liquidity Requirement Regulation of the B.C. Financial institution Act and equivalent ON legislation, and as a contingent funding source. Jumping to 2021, substantially all B.C. and ON credit unions likely now have portfolios of fixed income securities, held in legally ring-fenced trust accounts, on their balance sheets. Forget proportionality. Regulatory changes impacted the largest and smallest credit unions alike. Identical regulatory reporting requirements and frequency. Hopefully Canadian consumers can sleep a lot more easily each night, safe in the knowledge that their cooperative financial institution has lower systemic liquidity risk due to it directly holding a ring-fenced portfolio of high quality liquid assets. Or not. Retail banking, it seems, is a whole lot more complex than it used to be.

‘Forget proportionality. Regulatory changes impacted the largest and smallest credit unions alike. Identical regulatory reporting requirements and frequency. ’ - Ross McDonald

Credit unions should reflect on unpleasant realities. Fixed income securities, once the domain of second-tier entities and wholesale banks, are new to substantially all credit unions and executives. Regulatory guidelines, prudential supervisory expectations, and regulatory reporting in regards liquidity management have escalated to a level unimaginable only a few years ago. This new world seems a permanent, irreversible change. It may contribute to collaboration, amalgamation or other strategic discussions. Any credit union that fails to duly adapt is likely to experience the relentless intervention wrath of its financial regulator.

In the spirit of cooperative values and wiser together, below are several treasury tactic ideas that smaller credit unions may consider in regards statutory liquidity deposits.

First, consider radical simplification. In January 2021, Central 1 Credit Union terminated legacy term deposits and migrated equivalent portfolio of fixed income securities. This provided member credit unions with duly equivalent exposure. Credit unions may continue in this way. But there is no such compulsion. Central 1 Credit Union, and its peers, are now service providers to be duly instructed. Credit unions have discretion in selection of asset manager and in the establishment of related investment strategy. Academic research highlights the ‘cost of complexity’. Were it so inclined then a credit union could consciously instruct its asset manager to discard all fixed income securities and hold familiar bank deposits, provided that they satisfy HQLA criteria. Perhaps lesser yields may result. But the potentially material simplification of accounting journals, risk management and/or resourcing costs could make such an approach attractive. This approach aligns with strategic practice of choosing ‘where-to-play’. Perhaps treasury, for some smaller credit unions, is somewhere not-to-play. K.I.S.S. is a timeliness axiom for a reason.

‘a credit union could instruct its asset manager to discard all fixed income securities and hold familiar bank deposits, provided that they satisfy HQLA criteria’ - Ross McDonald

Second, constrain portfolio scope. Many types of securities qualify as High Quality Liquid Assets. A regulator may recommend, or require, that an Investment and Lending Policy provide detailed criteria of securities attributes (e.g. credit rating) for each security type. For example, if ILP states that corporate bonds are acceptable as a security type then it may need to state which issuers, industries, credit ratings or other attributes are acceptable or unacceptable. A credit union may determine that some potential HQLA security types are undesirable. Maybe the credit rating specification is unfamiliar. Or perhaps the accounting journals are troublesome. A credit union may direct its asset manager not to hold corporate bonds, mortgage backed securities or another type of HQLA. This approach may align with the concept of competitive advantage. Perhaps being good-enough at treasury management is just that - good enough.

Third, evolve oversight. Finance & Risk reporting should include Liquidity Adequacy Ratio. Prudential supervisors appear to have sharpened their liquidity compliance. The legacy broadly defined Statutory Liquidity Ratio has been effectively replaced by a more restrictive Liquidity Adequacy Ratio. Most liquidity held by a credit union outside of the in-trust account(s) does not count towards its compliance with legislative requirements. As part of ‘Quality of Risk Management’, assessment prudential supervisors may be re-reviewing executive expertise and board oversight of liquidity management. This approach may align with measuring what matters. Your friendly regulator may have said that LAR% now matters.

‘As part of Quality of Risk Management assessment, prudential supervisors may be re-reviewing executive expertise and board oversight of liquidity management.’ - Ross McDonald

Fourth, expectation management. Despite commendable enthusiasm, executive/board committees and boards may be content to receive limited reporting on key finance & risk topics. At least for an initial period. Reporting from an asset manager, custodian or other service provider may well be evolving in its rigour, scope or timeliness. Trailblazing credit union executives may have already designed comprehensive internal reporting. Smaller credit unions likely have not. Patience can be a virtue, and may save duplicated effort. Whether as part of mandated work scope; a response to industry feedback; or to mitigate threats from circling competitors then asset manager and/or other service providers have every incentive to provide appropriate reporting at their earliest convenience.

Fifth, professional development. Treasury competences are now cool in credit unions. Who’d have ever guessed that! Executive Asset & Liability Committees and board Investment & Lending Committees may find unfamiliar and elevated stakeholder attention. Some finance executives may need to brush up on technical knowledge of financial instruments. Or to initiate accelerated training. Scary times perhaps. Finance executives with a growth mindset may view HQLA as a wonderful opportunity to expand product knowledge; to extend functional maturity; and to better serve the business and membership. Executives with a curious mindset may ask ‘dumb’ questions about how liquidity, risk, return and cashflows impact their organization. This approach may align with functional maturity. Given changes in external environment, some credit unions may re-evaluate their current and target levels of functional maturity for Finance or treasury. Financial regulator(s) may have moved the goalposts. Time to recalibrate.

‘internal stakeholders may be content to receive limited reporting on key finance & risk topics in regards HQLA, at least for an initial period.’ - Ross McDonald

Lastly, seek help. Sometimes we all need a little help from our friends. As appropriate, reach out to peer credit unions for advice. Or seek a paid contractor relationship with a credit union that has relevant expertise. B.C. credit unions may request the assistance of Stabilization Central Credit Union. Or explore support from service provider(s).

Make no mistake, prudential supervisors may well dispense some unpleasant letters. Remediation from a regulatory intervention is a thoroughly unpleasant place. Credit unions may mitigate regulatory risk through proactive adaptation of liquidity management practices, rather than naively hoping for the best.

During the pandemic, many executives and staff have been working from home. The presence of domestic pets may provide welcomed comfort and companionship. A wagging dog tail; a purring cat; a chirping bird; or otherwise may bring joy and smiles. Such selfish pleasures may be repaid through fewer expletives from their owners.

DISCLAIMER & COPYRIGHT

This article reflects the personal opinions of the author, Ross McDonald. This article does not represent the views of any financial cooperative, corporate organization, regulatory body, government ministry or other organization. All content is wholly based on information that is in the public domain. Where relevant, sources have been identified and referenced.

Although the author has made significant effort to ensure that the information in this submission was accurate at the date of completion then the author does not assume any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

Proportionality in financial regulations. Asset size, business complexity & risk profile should matter.

Financial regulation is not national security. Edward Snowden alleged that 'collect it all' was a mantra of the US National Security Agency. But this seems rather heavy-handed for regulatory oversight of provincial credit unions. As a self-declared 'data-driven regulator', BC Financial Services Authority appears intent on data collection regardless of prudential supervisory risk or industry impact.

Financial regulation is not national security. Edward Snowden alleged that 'collect it all' was a mantra at the U.S. National Security Agency. But this seems rather heavy-handed for regulatory oversight of small provincial credit unions. As a self-declared 'data-driven regulator', BC Financial Services Authority (BCFSA) appears intent on maximum data collection regardless of its supervisory framework and industry consequences.

A formatted PDF of this article is available at https://www.bitly.com/rm-proportionality.

Following the 2008 financial markets crisis, regulators of major global banks duly turned up the heat. New mechanisms were designed and introduced to assess the capital, liquidity and risk profile of regulated financial institutions. Entities that regulators deemed 'too-big-to-fail' or 'globally systemically important banks' (G-SIB) were exposed to incremental costs, being higher compliance costs that were commensurate with their regulatory risk profile. These reporting requirements and supervisory expectations have steadily trickled down to domestic equivalents (D-SIB) and, in Canada, to provincially regulated financial institutions. The extent of due adaptation of G-SIB regulatory requirements for small community credit unions seems variable. Copy-and-paste can be a dangerous tool.

The regulatory environment for B.C. credit unions is wholly unrecognizable from a decade ago. Over recent years then BCFSA - and its predecessor FICOM - introduced numerous regulatory guidelines; escalated prudential supervisory expectations; and intensified regulatory reporting. The number, diversity and complexity of these new regulations are dizzying. By way of illustration, in late 2020, BCFSA launched an overhaul of regulatory reporting requirements for credit unions. The proposal seeks to expand data scope; introduce greater data granularity; on a more frequent basis; and from an increased number of credit unions. As regulated entities, B.C. credit unions have but three choices - comply, strategic transformation, or federal charter.

"The intensity of supervision will depend on the nature, size, complexity and risk profile of a PRFI.” - BCFSA Supervisory Framework

BCFSA appears to have discarded FICOM’s risk-based supervisory framework. Default prudential supervision, and regulatory reporting, was relatively modest. But credit unions of larger size, greater complexity and/or intervention stage rating should be subject to commensurately escalated intensity of prudential supervisory requirement and regulatory reporting. Following a flurry of new regulatory requirements then this approach - proportionality - is now being embraced by OSFI, a federal Canada financial regulator. BCFSA should take note. Instead, BCFSA seems intent on a wholly opposite approach - standardization. Vancity Credit Union (C$23 billion assets) and Vancouver Police Credit Union (C$18 million assets) have order-of-magnitude organizational differences, yet BCFSA proposed regulatory reporting would impose substantially similar regulatory reporting requirements. As would credit unions with scarcity or bountiful levels of capital or liquidity. As would credit unions with low-risk or high-risk intervention stage ratings. The objective of regulatory reporting should be to ensure legislative compliance and to assist prudential supervisory assessment of composite risk rating. This risk-based approach wholly aligned with its supervisory framework. No matter. Collect it all. Fill those databases.

"One of the key priorities identified in OSFI's Strategic Plan 2019-2022 is to further adapt its regulatory approaches to reflect the size, complexity and risk profile of financial institutions.’ – Source: OSFI ‘Advancing Proportionality: Tailoring Capital and Liquidity Requirements for Small and Medium-Sized Deposit-Taking Institutions'

BCFSA should stop and think. What is the purpose of the collected data? Why do the proposed changes fall disproportionally on credit unions with less than C$1 billion assets? How will the proposed changes have intended and/or unintended consequences on B.C. credit unions?

BCFSA should consider alternative tactics. Perhaps there could be two sets of 'standardized' regulatory reports - a simple set and a comprehensive set. This may mirror efforts in accounting standards - small, private enterprises and large, publicly listed companies produce financial statements of differing complexity. The Financial Accounting Standards Board 'Simplifying Accounting Standards' is exploring various topics related to proportionality in application of accounting standards. Perhaps there are learnings from the U.S. Federal Reserve, that has four intensities of regulatory reporting for deposits based on financial institution size. Perhaps B.C. credit unions could have an opt-in approach with a distant date rather than a near-term effective date (hat tip to peer for this pragmatic idea). Such an approach would allow smaller credit unions to consider banking system changes, resourcing requirements and/or strategic viability of the proposed changes. Perhaps CUDIC excess capital could be rebated, say on an equal dollar value basis across B.C. credit unions, to help fund process improvements, system implementation or other necessary automation to satisfy elevated reporting requirements?

BCFSA should recognize that there are multiple, diverse & complex changes impacting B.C. credit unions. BCFSA-required transformation of statutory liquidity deposits. Central 1 and membership driven implementation of digital technologies. BCFSA new supervisory expectations, such as the January 2021 Liquidity Guideline. At this time, BCFSA has four active consultations with credit unions - regulatory reporting, CUDIC assessments, IT Security, Outsourcing. Some requirements may even be competitive. For example, if credit unions respond the proposed regulatory reporting by sharing expert resource then this may create resource dependency and outsourcing risk. But if credit unions respond by recruiting dedicated staff or investing in technology then this will impact prudential supervisory assessment of earnings risk. Credit unions less than C$1 billion assets face a lose-lose situation.

“It certainly seems possible that BCFSA consequences and Competition Bureau objectives, as they relate to credit union amalgamations, may be significantly misaligned.” - Ross McDonald

Collectively these, mostly BCFSA driven, changes will permanently impact the B.C. credit union system. Ultimately, ever-increasing baseline regulatory requirements must surely translate into fewer provincial credit unions and increased minimum efficient scale. Should BCFSA continue on its seeming path, there may be only a residual few B.C. credit unions with less than C$1 billion assets by 2025, and perhaps none by 2030. A torrent of amalgamations seems inevitable. Per related member website, the ongoing proposed merger by six B.C. credit unions has been referred to the Competition Bureau. It certainly seems possible that BCFSA consequences and Competition Bureau objectives, as they relate to credit union amalgamations, may be significantly misaligned.

Do-as-I-say, not do-as-I-do. As part of the Ministry of Finance, FICOM reporting to industry was negligible, if anything. As a crown corporation, time will tell if BCFSA complies with the B.C. government 'Performance Reporting Principles For the British Columbia Public Sector'. The related publication, approved by the Auditor General of B.C, frames eight principles of deemed best practice that seek to support an open and accountable government. BCFSA compliance with B.C. government reporting principles for crown corporations require it to provide comprehensive disclosures to industry and to taxpayers. People who live in glass houses shouldn't throw stones.

“BCFSA compliance with B.C. government reporting principles for crown corporations require it to provide comprehensive disclosures to industry and to taxpayers.” - Ross McDonald

BCFSA executive has the near infinite authority over its expanded empire. Oversight lies in its board of directors, and ultimately the B.C. Ministry of Finance. Under the Taxpayer Accountability Principles of the B.C. government state that ‘Board members act independently from the organization’s executive and have the best interests of taxpayers and shareholder as their primary consideration.' Hopefully this enshrines expectations of a principal-agency relationship. Approximately 40% of British Columbians are members of B.C. credit unions. Collectively B.C. credit unions provide substantial benefit to their members, employees, communities and the B.C. economy. BCFSA Board should ask difficult questions of the executive team; demand a business case for proposed changes; and consider the collective impact on British Columbians.

In the short-term, BCFSA may amass a standardized, NSA-worthy database about B.C. credit unions. Probably significantly more than that required to fulfil the needs of executive management, board oversight or risk-based prudential supervision. In the medium term, this database may become a museum relic. A moment in time record of an industry that was subject to accelerated transformation and proactive consolidation by its regulator. A priceless collector’s piece but a needless lament.

___

REFERENCES

OSFI January 2020 'Advancing Proportionality: SMSB Capital & Liquidity Requirements - Consultatitve Document' - https://www.osfi-bsif.gc.ca/Eng/fi-if/in-ai/Pages/SMSB20_cp.aspx

OSFI July 2019 'Advancing Proportionality: Tailoring Capital and Liquidity Requirements for Small and Medium-Sized Deposit-Taking Institutions' - https://www.osfi-bsif.gc.ca/Eng/fi-if/in-ai/Pages/smsb.aspx

FICOM/BCFSA June 2012 'Supervisory Framework' -https://www.bcfsa.ca/pdf/aboutus/FICOMSupervisoryFramework.pdf

FASB 'Simplifying Accounting Standards' - https://www.fasb.org/simplification

B.C. Government 2003 - “Performance Reporting Principles” - https://www2.gov.bc.ca/assets/gov/british-columbians-our-governments/services-policies-for-government/public-sector-management/performance_reporting_principles.pdf

Member website for potential amalgamation of B.C. interior credit unions - https://www.exploringstrengthandunity.ca/awesometogether.html

U.S. Federal Reserve Reporting Requirements for deposit reporting: https://www.federalreserve.gov/monetarypolicy/reserve-maintenance-manual-reporting-requirements.htm

___

DISCLAIMER & COPYRIGHT

This article reflects the personal opinions of the author, Ross McDonald. This article does not represent the views of any financial cooperative, corporate organization, regulatory body, government ministry or other organization. All content is wholly based on information that is in the public domain. Where relevant, sources have been identified and referenced.

Although the author has made significant effort to ensure that the information in this submission was accurate at the date of completion then the author does not assume any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

All rights reserved.

FIA / CUIA - Empowering CUDIC - Beyond FICOM's Shadow

CUDIC has outgrown legacy legislation and FICOM’s shadow. CUDIC is responsible for deposit insurance of a C$77 billion industry that is used by almost half of British Columbians. Larger than most Canadian credit unions then it warrants full-time, permanent executive leadership. Larger than most B.C. Crown Corporations then it deserves independent, empowered and accountable governance oversight.

“CUDIC has outgrown legacy legislation and FICOM’s shadow. CUDIC is responsible for deposit insurance of a C$77 billion industry that is used by almost half of British Columbians. Larger than most Canadian credit unions then it warrants full-time, permanent executive leadership. Larger than most B.C. Crown Corporations then it deserves independent, empowered and accountable governance oversight.”

CONTEXT

The following submission was authored by Ross McDonald, in a personal capacity, in response to the Second Public Consultation Paper of a legislative review by the Ministry of Finance of the B.C. provincial government. Under the review, the Ministry of Finance sought public submissions by 19 June 2018. The legislative review considers changes to the Financial Institutions Act and the Credit Union Incorporation Act. This submission provides four recommendations on a targeted subset of relevant topics. Recommendations per this submission are aligned with stated legislative objective and collectively offer policy ideas that have the potential to courageously transform the regulatory environment of B.C. credit unions for the benefit of industry, government, taxpayers and employees.

Ross wishes to thank various credit union system veterans that kindly volunteered leadership inspiration, technical insight and professional encouragement. Thank you, appreciated.

This submission may be easier to read in PDF format. Download per bit.ly/fia-cuia-rm-pdf

EXECUTIVE SUMMARY

This personal submission to the FIA/CUIA Review seeks to frame an alternative regulatory structure for B.C. credit unions. Specifically, the submission provides four recommendations:

Recommendation 1 - Roles & Responsibilities

Transfer the mandate for prudential supervision, including completion of risk-based assessments and determination of deposit insurance premiums, of B.C. credit unions and credit union centrals from FICOM to CUDIC. Terminate any requirement that CUDIC be administered by FICOM.

Recommendation 2 - Legal Entities

Establish CUDIC as a Crown agency. Retain FICOM as branch of the Ministry of Finance. Collaborate with industry to review the legislative mandate, appropriate sustainable resources, and any potential merger of Stabilization Central Credit Union.

Recommendation 3 - Leadership & Governance

Appoint permanent executive and an independent, empowered governance body to provide leadership and oversight of CUDIC. Related competency matrices and governance processes should reflect CUDIC financial size, technical complexity and systemic role. CUDIC Board should adopt, and strive for excellence in, relevant governance best practices.

Recommendation 4 - Public Accountability

Regardless of their legal entity structure then FICOM and CUDIC should, as separate organizations, be subject to the “Performance Reporting Principles” and “Taxpayer Accountability Principles” as published by the B.C. government.

The recommendations are aligned with the primary objective of the legislative and regulatory framework “to maintain stability and confidence in the financial services sector by reducing the risk of failures and providing consumer protection and supporting objectives.” Related execution would necessitate short-term legislative change and organizational restructuring. Some portion of this work may be already actively engaged given the initial recommendations by the B.C. Ministry of Finance.

The recommendations recognize the current size, elevated complexity, resource challenges and peer jurisdiction approaches in regards regulatory oversight of credit unions. Recommendations may create significant benefits to government, to industry and to the public over a medium-term basis. Given numerous, diverse and substantive externalities that face the credit union industry, the recommendations may position the regulatory oversight for the coming decade until the next legislative review.

The author believes that credit unions contribute materially to the economy, employment and communities of B.C. This submission is motivated by personal appetite for a strong and sustainable B.C. credit union industry; for an effective, efficient and appropriate regulatory structure; for best practice adoption in regards governance oversight and public accountability.

RECOMMENDATION 1 - ROLES & RESPONSIBILITIES

Recommendation: Transfer the mandate for prudential supervision, including completion of risk-based assessments and determination of deposit insurance premiums, of B.C. credit unions and credit union centrals from FICOM to CUDIC. Terminate any requirement that CUDIC be administered by FICOM.

B.C. has the largest provincial credit union system in Canada. As at 31 December 2017 then B.C. credit unions reported C$77 billion of assets, C$66 billion of member deposits and 2.0 million members that represent over two-fifths of the provincial population. Three of the top five Canadian credit unions are located in British Columbia. The B.C. credit industry is growing. Between 2005 and 2017, B.C. credit union assets increased from C$36 to C$77 billion and membership increased from 1.5 to 2.0 million.

Over recent years, credit union operations have increased in complexity. Elevated consumer expectations, heightened competition and evolving technological innovation have necessitated significant investment by credit union organizations in digital channels, product offerings and operational efficiency. Increased scale may have permitted increased sophistication by larger B.C. credit unions. For example, between December 2007 and 2017, the total assets of Vancity Credit Union increased from C$14.1 to C$21.7 billion (Source: Vancity CU).

The B.C. credit union industry and its regulator gained national, systemic impact. In recognition of its importance to Canadian credit unions then, in 2014, FICOM designated Central 1 Credit Union as a Domestically Systemically Important Financial Institution. As such, it subject to commensurately elevated regulatory requirements and prudential supervisory expectations. Between 2005 and 2017, Central 1 Credit Union assets increased from C$5 to C$18 billion. While asset growth includes a 2008 merger with Credit Union Central of Ontario then the majority of asset growth was driven by higher member deposits at B.C. credit unions. As of 1 January 2017, responsibility for regulatory oversight of Central 1 Credit Union passed from the federal Office of the Superintendent of Financial Institutions to FICOM. Central 1 Credit Union holds mandatory liquidity deposits for all B.C. and some ON credit unions. It provides wholesale payments, treasury and numerous other services to credit unions nationwide. The nature and complexity of its operations, and therefore its regulatory policies and prudential supervisory approach, are materially different from that of a credit union.

FICOM does not appear to have the operational capabilities to fulfil its mandate in regards credit union prudential supervision. In 2016, the BC Auditor General concluded that “FICOM may not be able to detect a worsening situation at a credit union in time to address and reduce the risk of failure.” This expert, independent determination strikes at the heart of the prudential supervision function. FICOM Supervisory Framework publication states that “the objective of FICOM’s supervision is to reduce the likelihood that a provincially regulated financial institution will fail.”

Over recent years, FICOM appears to have completed a very small number of supervisory reviews of credit unions. B.C. has 42 credit unions. The 2014 BC Auditor General report stated that “With their shortage of staff, it would take over 14 years to review all of BC’s credit unions instead of FICOM’s intended target of two to three”. It could be inferred that FICOM completed supervisory reviews of three credit unions (42 divided by 14), or equivalents thereof, each year. This compares to the 14 to 21 credit unions, or equivalents, that require prudential supervisory reviews annually to achieve FICOM’s target. The 2016 BC Auditor General report stated that “FICOM’s actions to address its staffing shortage are not working. FICOM has further reduced the number of credit union reviews it will do each year”. This suggests that FICOM prudential supervision team may review each credit union once every couple of decades or so. This frequency of review compares extremely poorly to regulatory standards in other jurisdictions and in other regulated industries. The lack of timely supervisory assessments of credit unions may increase deposit insurance risks for B.C. taxpayers, given current unlimited deposit insurance policy.

“FICOM may not be able to detect a worsening situation at a credit union in time to address the risk of failure.”

The extent of FICOM’s responsibilities are materially greater than those of peer provincial regulatory entities. FICOM regulates multiple industries - credit unions, trust companies, insurance companies, real estate, mortgage brokers, strata properties and pension plans. FICOM performs substantially all regulatory function for B.C. credit unions. Specifically FICOM - inclusive of CUDIC - is responsible for regulatory policy, statutory approvals, prudential supervision, deposit insurance and market conduct. Most, if not all, other Canadian provincial regulatory structures use multiple organizations to perform equivalent industry coverage and functional responsibilities.

Despite FICOM’s multi-year resource challenges, its authority was recently further extended. In 2017, the BC Ministry of Finance tasked FICOM with the new function of Office of the Superintendent of Real Estate, a seemingly prominent and impactful role given the substantive recommendations of the B.C. Government’s Independent Advisory Group.

The B.C. Ministry of Finance should revisit any business case that requires CUDIC to outsource its administration and/or operations to FICOM. The BC Ministry of Finance FIA/CUIA March 2018 recommendations state that “CUDIC was merged with FICOM in 1990 to allow expertise to be pooled; that pooling of expertise continues to be relevant and important today.” At that time then both FICOM and CUDIC were startup organizations, perhaps with an all-hands-on-deck mindset. But CUDIC and FICOM are now mature organizations. The rationale of pooled expertise between FICOM and CUDIC may reflect legacy pragmatism rather than current circumstances or future needs of the B.C. credit union industry and related regulation.

FICOM operational capabilities to set regulatory policy for credit unions appear effective under the current organizational structure. Since the prior FIA/CUIA review then FICOM has introduced, and updated, a significant number of regulatory guidelines. It has also progressed multiple adhoc initiatives, such as stress tests, in efforts to assess industry risk and/or to enhance credit union capabilities.

RECOMMENDATION 2 - LEGAL ENTITIES

Recommendation: Establish CUDIC as a Crown agency. Retain FICOM as branch of the Ministry of Finance. Collaborate with industry to review the legislative mandate, appropriate sustainable resources, and any potential merger of Stabilization Central Credit Union.

The size of CUDIC net income may warrant it being a standalone organization. For the year to March 2017, CUDIC net income of C$57 million. Such earnings are large relative to a) BC’s largest credit unions, b) aggregate earning of BC credit unions, and c) many BC Crown corporations. For comparison, Coast Capital Savings Credit Union reported C$58 million net income in the year to December 2016. In the same period, BC credit unions collectively reported net income of C$263 million. Over recent years then net income of CUDIC relative to that of BC credit unions has increased materially, from 13% to 22%, principally due to material increases in deposit insurance premiums. Investment returns from the CUDIC deposit insurance portfolio funds FICOM operations.

The size of CUDIC assets may warrant it being a standalone organization. Between December 2007 and 2017, CUDIC assets increased from C$230 to C$596 million (Source: CUDIC). CUDIC assets have grown materially through higher system deposits, elevated funding policy target and fund transfer.

The B.C. Ministry of Finance should revisit its seeming business case for FICOM’s expansive mandate scope and instead prioritize effective structure, functional excellence and public accountability. The BC Ministry of Finance should strive to identify, and to adopt, best practices in regards the regulatory structures for credit unions. With the exception of BC then most, if not all, regulatory structures in other Canadian provinces separate regulatory functions into multiple organizations. Typically, regulatory policy and statutory approvals are performed by a provincial government organization, while deposit insurance and prudential supervision are executed by a provincial crown corporation (commonly a ‘Credit Union Deposit Guarantee Corporation’).

CUDIC prudential supervision may enable a simple, transparent funding model. The B.C. credit union industry would directly fund the majority of regulatory costs, including prudential supervision activities, through deposit insurance premiums to CUDIC, while the B.C. Ministry of Finance and/or stakeholders would fund residual FICOM functions. Most, if not all, monetary transfers between CUDIC and FICOM, and between FICOM and the BC Ministry of Finance, would terminate. The current funding model may be needlessly complex and appears significantly different from practices in other provinces.

“The B.C. Ministry of Finance should revisit it seeming business case for FICOM’s expansive mandate scope and instead prioritize effective infrastructure, functional excellence and public accountability.”

Legal separation between FICOM and CUDIC may be beneficial to government, industry, taxpayers and employees. The competency matrix, staffing requirements and labour market rates across the regulatory functions likely vary materially. There may be some functions that are performed to a higher standard; with greater timeliness; or on a cost-effective basis by public servants employed by the B.C. Ministry of Finance. For example, public servant direct access to B.C. government resources may provide clarity of discussions towards better and/or more timely decisions for statutory approvals. B.C. Ministry of Finance may seek to have direct input - perhaps to partly mitigate its deposit insurance risk - into processes that introduce, edit, or alter the intensity of regulatory policies. Employees may benefit from legal separation of FICOM and CUDIC as some current FICOM employees may prefer to remain in the public service.

Risk assessment responsibility and related funding source were significantly migrated from industry to government. In 2005, the relationship between FICOM/CUDIC and Stabilization Central Credit Union (‘SCCU’) - an entity owned and governed by B.C. credit unions - was significantly revised and “this resulted in the Stabilization Fund being reduced by $83 million to approximately $30 million, with the CUDIC deposit insurance fund increased by a like amount.” (Source: SCCU 2005 Annual Report). “These new arrangements restrict the flow of information between Stabilization Central and FICOM/CUDIC, with the result that Stabilization Central’s role in assessing risk is more limited” (Source: SCCU 2005 Annual Report). The 2005 fund $83m transfer was transformative in size relative to then asset sizes of CUDIC and SCCU.

SCCU should be considered as part of any regulatory restructuring. SCCU has a legislative mandate to act as the stabilization authority to B.C. credit unions. SCCU - owned, governed and operated by industry - appears to provide a valuable force for betterment in the credit union system. It advises specific credit unions that voluntarily choose, or have been required by FICOM, to initiate organizational changes. It promotes best practices across B.C. credit unions. In an environment of increased complexity and elevated regulations then it may act as an informed, cost-effective and trusted counsellor to boards of directors of B.C. credit unions - especially those of small and medium size. Its role contributes to the mitigation of deposit insurance risk. Annual reports of, and the 2015 FIA/CUIA submission by, SCCU disclose deliberations by its board in regards organizational viability and potential merger partners. They also highlight significant desire for a clearly defined, appropriately informed and credibly sustainable role. SCCU could play various future roles. Its functional responsibilities could be extended. Its legal status could remain as a standalone entity or be merged with Central 1 Credit Union or CUDIC. This submission does not consider related matters or propose specific recomendation(s). The B.C. Ministry of Finance should collaborate with industry to critically assess the business case, alternative strategic options, and effective future role of SCCU.

RECOMMENDATION 3 - LEADERSHIP & GOVERNANCE

Recommendation: Appoint permanent executive and an independent, empowered governance body to provide leadership and oversight of CUDIC. Related competency matrices and governance processes should reflect CUDIC financial size, technical complexity and systemic role. CUDIC Board should adopt, and strive for excellence in, relevant governance best practices.

By virtue of legacy legislation, CUDIC has never had dedicated executive leadership. The Superintendent of Financial Institutions also holds the official capacities of Superintendent of Pensions, Registrar of Mortgage Brokers, Superintendent of Real Estate plus CUDIC Chief Executive Officer. The CUDIC Executive Director, and limited CUDIC staff members, are FICOM employees. FICOM completes executive functions, such as establishment of the deposit insurance fund target policy, on behalf of CUDIC (Source: CUDIC annual report). FICOM staff provide significant operational services and administrative support to CUDIC.

For over two years, FICOM absence of permanent executive leadership has impacted CUDIC. Carolyn Rogers resigned as Superintendent of Financial Institutions in May 2016. Jeffrey Wu, Executive Director CUDIC, left FICOM at a similar date. Since that time FICOM has been led by an Acting Superintendent, Acting Superintendent Regulation, Acting Deputy Superintendent Prudential Supervision and Acting Deputy Superintendent Market Conduct. FICOM corporate functions are directed by an Interim CEO. Day to day operations of CUDIC are overseen by a FICOM employee that was appointed Acting Executive Director CUDIC.

CUDIC deserves full-time, permanent executive leadership:

its organizational size is larger than most B.C. credit unions and most B.C. crown corporations

its operating environment - the B.C. credit union industry - has increased materially in terms of size and complexity

its impact on supervisory risk assessments, and potential remedial interventions, to B.C. credit unions may be significant

its leadership competency matrix - including technical expertise, management skills and stakeholder relationships - may differ significantly from that required to set regulatory policy or assess statutory approvals

its responsibilities and resources, subject to above recommendations, may increase materially

By virtue of legacy legislation, CUDIC has never had dedicated governance oversight. Members of the FICOM Commission also act as Board Directors of CUDIC. As at March 2018, there were six appointed members of the FICOM Commission. It may be indicative of the conjoined relationship, of limited resourcing and/or of perceived functional priorities that CUDIC appears not to have submitted a response to the 2015 Initial Public Consultation Process of the FIA / CUIA consultation review. Were this the case then its Board of Directors should justify why CUDIC elected not to offer thought leadership, policy opinion and/or regulatory input on legislative matters at the core of its organizational purpose.

CUDIC Board may have mismatched competencies. Conjoined governance of FICOM and CUDIC implicitly requires compromise in appointee selection. Competency matrices are commonly used by a Board of Directors to balance its collective professional experience, environmental or contextual knowledge and personal attributes and skills. FICOM provides regulatory oversight for multiple industries including credit unions, insurance, trusts, pensions, real estate and mortgage brokers. FICOM Commission members presumably have appropriate expertise and experience across these industries, and understanding of related regulatory issues. Implicitly then only a subset of that expertise, experience and skills are relevant to credit unions and to CUDIC. Yet the CUDIC Board and FICOM Commission have identical membership.

Diverse conflict of interest requirements may limit the candidate pool for CUDIC Board. The Board Resourcing and Development Office related posting stated that “to be considered as a [FICOM] Commission member an individual must not have any real or perceived conflict of interest with the industries or institutions regulated by FICOM.” The conjoined governance structure therefore means that a candidate with a potential conflict of interest in the pension, mortgage broker, insurance or real estate industry is automatically prohibited from providing governance oversight of CUDIC and its credit union mandate.

CUDIC has outgrown legacy legislation and FICOM’s shadow. The size, complexity and impact of the B.C. financial services industry is material. Largely devised in the late 1980s then legacy legislation in regards leadership and governance of CUDIC may be outdated. CUDIC is responsible for deposit insurance of a C$77 billion industry that is used by almost half of British Columbians. Larger than most Canadian credit unions then it warrants full-time, permanent executive leadership. Larger than most B.C. Crown Corporations then it deserves independent, empowered and accountable governance oversight.

CUDIC Board should have the authority - and the resultant responsibility - to appoint and to assess its Chief Executive Officer and to develop executive compensation plans. Multiple governance experts identify CEO selection as a key function:

‘Selecting the chief executive officer and planning for CEO succession are among the most important responsibilities of a company’s board of directors.’ - Harvard Law School Forum for Corporate Governance & Financial Regulation ‘Advice for boards in CEO Selection and Succession Planning’

‘Choosing the next CEO is the single most important decision a board of directors will make.’ - Harvard Business Review, ‘The Art and Science of Finding the Right CEO’

‘During a CEO search process, boards might do well to keep their long knives sheathed because, in fact, real leaders are threatening to those intent on preserving the status quo’ - Harvard Business Review, ‘Don’t Hire the Wrong CEO’

CUDIC Board should demonstrate leadership to credit unions through its compliance with governance best practices.

RECOMMENDATION 4 - PUBLIC ACCOUNTABILITY

Recommendation: Regardless of their legal entity structure then FICOM and CUDIC should, as separate organizations, be subject to the “Performance Reporting Principles” and “Taxpayer Accountability Principles” as published by the B.C. government.

“Political accountability is the accountability of the government, civil servants and politicians to the public and to legislative bodies”

Governance bodies that oversee public service organizations are typically obligated to publish service plans, annual reports and other documents to public stakeholders. Disclosures may be driven by legislative requirement, government expectations or voluntary engagement.

Substantially all Canadian financial regulatory agencies appear to make extensive public disclosures. For example, Credit Union Deposit Guarantee Corporation - typically responsible for deposit insurance and prudential supervision functions in peer provinces - publish annual reports that are comparable to a public company. Such reports may contain some or all of audited financial statements; management discussion and analysis; CEO and Board reports; executive team profiles; governance practices; industry developments; regulatory updates; supervisory performance metrics; and/or executive compensation.

Public disclosures by FICOM and/or CUDIC appear to be negligible. Neither FICOM nor CUDIC publish an annual report or similar document that provides insight and rationale into goals, achievements, risks, key decisions, financial performance and/or other information. CUDIC publishes limited annual financial statements. As a ministry branch, FICOM disclosures could potentially be provided in the service plans and other reports published by the B.C. Ministry of Finance. But the most current Annual Service Plan Report (2015-2016) published by B.C. Ministry makes no reference whatsoever in regards financial statements, performance metrics or any other information for either FICOM or CUDIC.

Regardless of their legal entity structure, both CUDIC and FICOM should initiate compliance with the B.C. Performance Reporting Principles. In 2003, the B.C. government established “Performance Reporting Principles For the British Columbia Public Sector”. The related publication frames eight principles of deemed best practice that were approved by the Auditor General of B.C. The principles seek to support an open and accountable government.

FICOM should dislose, and provide credible rationale, to industry and to the public its plan to achieve key organizational goals. For example, the 2018/19 to 2020/21 Service Plan of the B.C. Ministry of Finance establishes a performance target for FICOM that, in 2017/18, 85% of financial institutions have a supervisory assessment completed in the prior three years.

In June 2014 “Taxpayers Accountability Principles”, the B.C. government introduced a new expectation “for deputy ministers ... to hold the entity [B.C. public service organization] accountable for the outcomes and measurements identified by the minister responsible, in consultation with the respective board chair.”

Executive leadership is obligated to make difficult decisions. This is the case in industry, government and communities. Some decision may involve topics that have high complexity, elevated sensitivity, material implications, accelerated timeline and/or significant subjectivity. Decisions may impact the organization, employees, communities and other stakeholders. Decisions may be made with imperfect information, unknown external forces and without the benefit of hindsight. Regardless, executive leadership and related governance body should be accountable to stakeholders for the resulting outcomes.

“The Taxpayer Accountability Princples state that ‘Board members act independently from the organization’s executive and have the best interests of taxpayers and shareholder as their primary consideration.’”

For example, FICOM executive and governance body should be accountable for decisions to return millions of dollars to B.C. general revenues rather than spend it on mandate fulfilment and/or operational betterment. Related funds were ultimately sourced from credit union deposit insurance premiums. Gerry Kyllo, MLA, neatly captured the situation in a Select Standing Committee - observing that FICOM executive faced multiple options and, regardless of whether “it’s a wrong decision”, a distinct choice was made. That such disclosures result from adhoc testimony to public officials rather than from routine stakeholder engagement processes may conflict with the intent of the Taxpayers Accountability Principles. Respectful of their primary consideration, FICOM Commission should routinely report to the public details of important goals, decisions and perfomance of FICOM and provide related rationale on how it perceives key aspects to reflect the best interests of taxpayers.

The funding basis and governance model of credit union regulation may be subject to a principal-agent gap. Despite industry funding FICOM/CUDIC operations then its contribution to related governance, and its receipt of perfoamnce disclosures, are both minimal and contary to practices in peer provinces. Lack of industry participation in oversight may have denied due challenge to FICOM Commission and executive. The 2015 submission to the FIA/CUIA consultation process by the B.C. credit union system noted that “as the funder of CUDIC, credit unions should have a greater voice in its governance.”

REFERENCES

Selected Deposit Insurance Organizations

CUDIC (BC) - http://www.cudicbc.ca

CUDGC (AB) - http://www.cudgc.ab.ca

CUDGC (SK) - https://www.cudgc.sk.ca/about-us/

DGCM (MB) - http://depositguarantee.mb.ca/home/

DICO (ON) - http://www.dico.com

CDIC (Federal) - https://www.cdic.ca

Stabilization Central Credit Union - https://www.stabil.com/

Government References

FICOM - Supervisory Framework - https://www.fic.gov.bc.ca/pdf/aboutus/FICOMSupervisoryFramework.pdf

B.C. Government - “Taxpayer Accountability Principles” - https://www2.gov.bc.ca/assets/gov/british-columbians-our-governments/services-policies-for-government/public-sector-management/taxpayer-accountability-principles.pdf

B.C. Government - “Performance Reporting Principles” - https://www2.gov.bc.ca/assets/gov/british-columbians-our-governments/services-policies-for-government/public-sector-management/performance_reporting_principles.pdf

BC Select Standing Committee on Public Accounts - Draft minutes, October 2016 - https://www.leg.bc.ca/documents-data/committees-transcripts/20161005am-PublicAccounts-Vancouver-Blues

B.C. Ministry of Finance - “2015/16 Annual Service Plan Report” - http://www.bcbudget.gov.bc.ca/Annual_Reports/2015_2016/pdf/ministry/fin.pdf

B.C. Ministry of Finance - “2018/19 – 2020/21 Service Plan” - http://bcbudget.gov.bc.ca/2018/sp/pdf/ministry/fin.pdf

Federal Department of Finance and Treasury Board of Canada - “Directors of crown corporations: an introductory guide to their roles and responsibilities” - http://publications.gc.ca/collections/collection_2016/fin/BT77-1-1993-eng.pdf

Statistics Canada - 2016 Census data - https://www12.statcan.gc.ca/census-recensement/2016/dp-pd/hlt-fst/pd-pl/Table.cfm

Sources Referenced in Submission

Canadian Credit Union Association - Top 100 Credit Unions, Q4 2017 - https://www.ccua.com/~/media/CCUA/About/facts_and_figures/documents/Largest%20100%20Credit%20Unions/top100-4Q17_12-Apr-18.pdf

Canadian Credit Union Association - System Results, Q4 2017 - https://www.ccua.com/~/media/CCUA/About/facts_and_figures/documents/Quarterly%20National%20System%20Results/4Q17SystemResults_14-Mar-18.pdf

Harvard Law School Forum on Corporate Governance and Financial Regulation, ‘Advice for boards in CEO Selection and Succession Planning’ - https://corpgov.law.harvard.edu/2012/06/11/advice-for-boards-in-ceo-selection-and-succession-planning/

Canadian Coalition for Good Governance - ‘Building High Performance Boards’ - https://www.ccgg.ca/site/ccgg/assets/pdf/building_high_performance_boards_august_2013_v12_formatted__sept._19,_2013_last_update_.pdf

McKinsey & Company - “The CEO Guide to Boards” - https://www.mckinsey.com/featured-insights/leadership/the-ceo-guide-to-boards

FIA/CUIA System Response - http://www.fin.gov.bc.ca/pld/files/BC%20Credit%20Union%20System%20Response.pdf

Wikipedia - Accountability - https://en.wikipedia.org/wiki/Accountability

DISCLAIMER & COPYRIGHT

This article reflects the personal recommendations and statements of the author, Ross McDonald. It is wholly intended to assist the B.C. Ministy of Finance as part of the FIA/CUIA Public Consultation. This article does not represent the views of any financial cooperative, corporate organization, regulatory body or government ministry. All content is wholly based on information that is in the public domain. Where relevant, sources have been identified and referenced.

Although the author has made significant effort to ensure that the information in this submission was accurate at the date of completion then the author does not assume any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

All rights reserved.

Credit Union Deposit Insurance Policy - 2/2 - Costs, Benefits & Regulation

There are seemingly three policy options for deposit insurance for B.C. credit unions - Maintain unlimited coverage, Reintroduce limited coverage, Seek provincial alignment. There does not appear a right or wrong policy. But there are policy choices and resultant implications for the B.C. credit union system.

“There are seemingly three policy options for deposit insurance for B.C. credit unions - Maintain unlimited coverage, Reintroduce limited coverage, Seek provincial alignment. There does not appear a right or wrong policy. But there are policy choices and resultant implications for the B.C. credit union system.”

SERIES OVERVIEW

This article is the second part of a two-part series related to deposit insurance applicable to Canadian credit unions.

Overview, History & Pros/Cons: Policy in B.C. & Canada. Unlimited vs limited

Implications & Options: Benefits, cost & regulatory impact. Three policy choices

This series was substantially authored to aid an executive search process. Several system veterans kindly volunteered technical expertise, system memory, and professional guidance. Thank you. Their wisdom, perspective and encouragement were invaluable.

The first article introduced deposit insurance; outlined policy in multiple jurisdictions; and summarized generic pros/cons of limited vs unlimited deposit insurance policies.

This second article has two broad components. First, the implications of unlimited deposit insurance in terms of benefits, costs and regulation. Second, three discrete policy options and recent public positions of the B.C. credit union system. Given subject matter complexity, subjectivity and sensitivity then the author has leveraged significant graphical analysis in efforts to enhance explanation and to aid assessment. Some presented data is marginally stale but this is not believed to impact key themes.

This publication may be easier to read in PDF format. Download per http://bit.ly/dep-ins-pdf

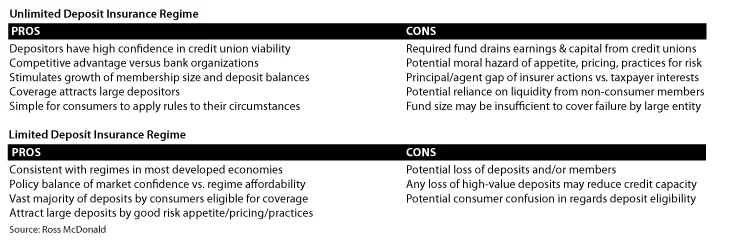

IMPLICATIONS: BENEFITS OF UNLIMITED DEPOSIT INSURANCE

The benefits to B.C. credit unions of a regime of unlimited deposit insurance are broad in nature, and may include -

Market confidence - Growth in collective membership size and deposit amounts at B.C. credit unions

Large depositors - Growth in number or magnitude of deposits that exceeded insurance coverage in other jurisdictions

In-province deposits - Retention of deposits of B.C. members by B.C. credit unions

Depositor Eligibility - it permits institutional entities, such as MUSH (municipal, university, schools and hospitals), to make deposits. Such entities may require that a financial institution have unlimited deposit insurance or a credit rating

Policy simplicity - Members may easily apply unlimited deposit insurance to their circumstances

Between 2007 and 2016 then the B.C. credit union system expanded its membership and attracted larger depositors. System membership increased by over 300,000, from 1.6 to 1.9 million. B.C. member deposits increased from C$36 to C$63 billion. The average member deposit increased from C$22,000 to C$32,000. A range of economic, market and external factors are potential drivers but the dates are also concurrent with the introduction of unlimited deposit insurance. It is possible that unlimited coverage provided members with increased confidence to join, and place higher deposit amounts, with B.C. credit unions.

Unlimited deposit insurance may provide a significant competitive advantage. Three Canadian provinces - BC, SK, MB - have credit union membership that represents in excess of 40% of the population. Each of these provinces has a regime of unlimited coverage. In contrast then Ontario credit union membership represents approximately 10% of its population. The modest market share of credit unions in Alberta and Ontario may be due to the likely strong competition from locally headquartered entities of ATB Financial and Canadian banks respectively.

“B.C. member deposits increased from C$36 to C$63 billion. The average member deposit increased from C$22,000 to C$32,000.”

Unlimited deposit insurance may have attracted larger depositors. At December 2015 then four provinces, each with unlimited coverage, have average credit union deposits in excess of C$30,000 while Ontario credit unions report less than C$25,000. Caution is appropriate with statistics. Higher average member deposit could indicate that many members have increased their deposits or suggest that a modest number of members, perhaps non-consumer, have placed outlier large deposits.

Limited data available in regards the retention of B.C. deposits in B.C. credit unions. It may be notable that, at December 2015, over half of the C$4.2 billion deposits at Concentra Financial were from Ontario customers.

IMPLICATIONS: COSTS OF UNLIMITED COVERAGE

Quantifying the cost of unlimited deposit insurance is tricky. Unlike typical insurance products, the buyer cannot seek a quotation from an alternative service provider or consider costs under multiple coverage insurance terms. Quantifying alternative deposit regimes is beyond the remit of this brief article. But comparable metrics of deposit funds may provide insight -

Historical B.C. levels - Fund levels prior to the introduction of unlimited coverage for B.C. credit unions

Other ‘unlimited’ provinces - Fund levels in other Canadian provinces that offer unlimited deposit insurance

‘Limited’ coverage entities - Fund levels applicable to deposit taking institutions subject to limited deposit insurance

Following the introduction of unlimited coverage, the cost of deposit insurance increased materially. Between 2007 and 2016 then B.C. deposit insurance funding increased from 76 to 95 basis points of member deposits at credit unions. Per current insurer targets then funding is expected to reach 118 basis points by 2021. Higher basis point funding can be associated with an insurer perception of elevated expected loss, say from increased claim sizes (exposure at default) or higher probability of claim (probability of default) that may arise from unlimited deposit coverage or challenging economic conditions.

The B.C. policy may be funded to a lesser extent than funds in provinces with similar coverage. Three other Canadian provinces offer unlimited insurance and each has a higher level of fund size, in terms of basis points of than that of B.C. Relative to its peers then annual assessments may rise the greatest in B.C. as it is currently furthest from its target funding levels.

As is typical of insurance, the fund capital is proportional to insurable risk. For deposit taking institutions, such as credit unions, the size of ex-ante fund increases with the magnitude of insurable deposits and so indirectly by deposit insurance policy. Ontario credit unions, federal credit and banks are each subject to C$100,000 deposit insurance. Related deposit insurer funds are, in basis points terms, materially smaller than in any of the provincial funds that provide unlimited insurance.

“Following the introduction of unlimited coverage, the cost of deposit insurance increased materially.”

While the cost of unlimited coverage requires significant analysis, the author suggests a few ballpark frames of reference-

Were 2007 funding (76bp) effective in 2016 then B.C. credit unions may have an estimated C$100 million more capital

Were 2016 ex-ante funding metrics in B.C. consistent with Ontario then the B.C. funds could be smaller by almost C$200 million

The forecasted increase in target fund levels may account for approximately C$15 million of annual CUDIC assessments

Published 2012 target funding may require continuance or escalation of CUDIC assessments at 18% of system earnings

IMPLICATIONS: REGULATION AND DEPOSIT INSURER

The author considers that unlimited deposit insurance for B.C. credit unions includes discrete financial implications:

Large depositors* - Growth in number or magnitude of high-value deposits enables lending but may increase liquidity risk

Annual premiums* - Elevated exposure at default increases insurance assessments to build a larger investment pool

Opportunity cost* - A larger insurance fund dilutes current earnings and reduces capital adequacy of credit unions

Market confidence** - Growth in membership size and deposit amounts at B.C. credit unions

In-province deposits** - Policy competitiveness encourages retention of deposits of B.C. members by B.C. credit unions

Regulatory compliance** - Insurance risk supports regulatory guideline issuance and supervisory expectation intensity

* High probability, ** Medium probability (author assessment)

CUDIC 2016 assessments represented 18% of the net income of the B.C. credit union system. This proportion is up from 14% in 2014. CUDIC assessments appear to wholly increase its investment asset pool. Between 2014 and 2016 then CUDIC investment portfolio returns have exceeded all expenses and taxes. CUDIC expenses include approximately $5 million charged, but significantly unspent, by FICOM. Deposition by Tara Richards, FICOM Acting CEO, to the B.C. Legislative Assembly states that ‘with the shortage of staff, we have a surplus ... of $3.5 million to $5 million on an annual basis. Last year [to 31 March 2015], for the record, the recovery [unspent income returned to B.C. government general fund] was $4.8 million’.

The B.C. ex-ante deposit insurance funds have increased in size relative to the aggregate capital of B.C. credit unions. In 2007 then the asset pools represented 12.2% of system capital but this had increased to 14.6% in 2016. Were the equity of Coast Capital Savings Credit Union excluded, assuming its future achievement of federal charter without CUDIC coverage, then the insurance asset pools would represent almost 20% of system. Payments by B.C. credit unions to CUDIC reduce their net income and, over time, retained earnings and capital adequacy.

In recent years regulatory compliance costs of B.C. credit unions may have increased materially. Based on the substance and frequency of regulatory guidance issuance the level of oversight appears to have expanded at an ever greater rate. Between 2013 and 2016 FICOM issued seven Guidelines; required extended reporting on various topics; and executed several system-level initiatives, such as stress tests. Some Guidelines issued by FICOM have resulted from task force or other consultative processes that involved executives, board members or advisors from B.C. credit unions.

CONCLUSION: POLICY OPTIONS

Option 1 - Maintain current unlimited deposit insurance regime

The current regime may have supported growth, reinforced strength and showcased confidence within the B.C. credit union system. During the current regime period then membership size and deposit amounts collectively at B.C. credit unions have increased by 19% and 72% respectively. Unlimited insurance appears to have attracted larger depositors, with average member deposits increased by 45%. System capital has increased by 78%. All Western Canadian provinces offer unlimited coverage.

The B.C. credit union system and most individual credit unions to be materially supportive of the current regime.

But an elevated level of moral hazard may enable inappropriate risk appetite, insufficient risk management or unsound business practices by B.C. credit unions. The regime is increasingly expensive. Assessments drain 18% of credit union system earnings. The ex-ante funds represent almost 15% of system capital. Regulatory requirements have intensified and compliance costs increased. Unlimited insurance may be acutely costly for credit unions under regulatory intervention.

Option 2 - Reintroduce a limited deposit insurance regime

Many depositors may want rather than need unlimited deposit insurance. Deposit taking institutions with limited deposit insurance have significant levels of uninsured deposits. 30% of deposits in Ontario credit unions are uninsured by DICO. 72% of deposits in banks and federal credit unions are uninsured by CDIC. Yet DICO and CDIC regimes currently apply maximum coverage of C$100,000 per depositor per account type. Per its federal credit union disclosures, fewer than 4% of personal members of Coast Capital Savings Credit Union have deposits that exceed CDIC's limited policy coverage.

The author understands that the current deposit insurance regime was introduced by the B.C. government as a surprise to, rather than at the request of, the B.C. credit union system. The re-introduction of limited deposit insurance could boost credit union earnings, redeploy system capital, simplify consumer expectations and/or ease regulatory burden. This may be welcomed given significant financial margins compression; elevated member expectations and technology investment; the system FIA/CUIA submission theme of ‘every bit of capital counts’; and 2014 and 2016 Auditor General of B.C. findings of resource challenges at the provincial regulator. Credit unions may ensure their adoption of sound risk management practices.

But limited coverage could negatively impact B.C. credit unions. Members with large deposit balances, market confidence sensitivities or depositor profile requirements may migrate their deposits outside of B.C. credit unions. The potential impacts of any material withdrawals from the B.C. credit union system include lending capacity, liquidity position, earnings potential and/or economic growth. Any regime transition need be carefully implemented and thoughtfully communicated to both B.C. credit unions and to their membership.

Option 3 - Seek alignment of deposit insurance regimes across provincial jurisdictions

Few, if any, significant jurisdictions outside Western Canada have deposit insurance regimes that provide unlimited coverage. Some jurisdictions introduced unlimited coverage regimes to consciously have a temporary impact. Credit unions in Ontario, Quebec and Atlantic Canada; all Canadian banks and federal credit unions; and most, if not all, deposit taking institutions in Europe and U.S.A. operate in deposit insurance regime with limited coverage. Federal credit unions will likely gain traction.

There may be an opportunity to concurrently align deposit insurance regimes in Canada. Any use of a deposit insurance regime to attract out-of-province deposits may be contrary to the principle of ‘cooperation among cooperatives’, may encourage in a race-to-the-bottom policy mindset, and/or may concentrate risk within provincial systems with the highest risk appetite. A regime could potentially distinguish between insurance coverage for members that reside in-province versus out-of-province.

But such changes would likely be complex, political and lengthy. Related regimes are enacted in provincial policy design and legislative execution would require buy-in from multiple provincial governments and demand extensive system resource. Some provincial credit union systems may be significantly adverse to the policy concept. A consistent regime between both credit unions and banks is likely infeasible, partly as large Canadian banks are effectively too-big-to-fail.

CONCLUSION: B.C. CREDIT UNION SYSTEM VIEW

Submissions to the B.C. Ministry of Finance FIA/CUIA review provide insight into the related views of B.C. credit unions.

Individual credit unions

The B.C. Ministry of Finance website in regards the FIA/CUIA Consultation process provides weblinks to submissions by ten individual credit unions. This represents approximately one-quarter of the number of B.C. credit unions, and likely a significantly higher proportion of its membership and deposits.

“Input Received from Stakeholders’ document notes that “Overall, most individual credit unions making submissions expressed strong support for retaining unlimited deposit insurance.”

One B.C. credit union, Community Savings Credit Union, provided significant critical commentary and provided details of its historical CUDIC assessments, that increased by 575% between 2008 and 2014. Its submission highlights the ‘subjective assessment by FICOM’ and the 2012 CUDIC methodology change as key related drivers, in addition to the typical impact of increased aggregate member deposit balances.

B.C. credit union system

The credit union system submission reiterates its prior stance in support of a regime of unlimited deposit insurance.

‘The system is thus still united in its position from the last substantive legislative review where it argued “as integral components of their communities and their regional economies, credit unions have played a ... role in providing financial services to public bodies. Each of these public bodies is responsible for raising and administering public monies.'

Further, the system response makes an express recommendation that 'the deposit insurance regime must respect the following five principles:

Maintenance of a competitive credit union system;

Supports provincial money staying in the province;

Recognizes the value of self-regulation in the system;

Is easily understandable by depositors; and

Any transitions must be well thought out and very carefully managed.'

“[B.C.] credit unions had unlimited deposit insurance between 1968-1988 with no evidence of problems.”

CONCLUSION: RECOMMENDATIONS

The author suggests that deposit insurance policy is neither a question of right or wrong, nor of decisions on isolated topics. But rather of choices and their collective implications to all stakeholders. Would B.C. credit unions be more inclined to advocate for limited deposit insurance if it were accompanied by lower CUDIC assessments, rebated CUDIC capital, aligned jurisdictional policies and/or lesser regulatory intensity?

This report is intended as a discussion document. The author expresses no opinion and proposes no recommendation.

This concludes the second article of a two-part series. For reasons of brevity, this report does not significantly consider related implications of current and emergent federal credit unions; the legislative history in jurisdictions other than B.C.; the mandate fulfilment by B.C. deposit insurer(s); the value-for-money of relevant services; or the funding levels, roles and responsibilities, or other matters between CUDIC and SCCU.

REFERENCES

B.C. Deposit Insurance Organizations

CUDIC: Guide to BC Credit Union Deposit Insurance - http://www.cudicbc.ca/pdf/cudic/CUDICGuide.pdf

CUDIC: Target Fund Policy - http://www.cudicbc.ca/pdf/cudic/TargetPolicy.pdf

CUDIC: 2016 Annual Report - http://www.cudicbc.ca/pdf/cudic/CUDICFinancials2016.pdf

Stabilization Central: Annual Reports - https://www.stabil.com/about/

Other Selected Deposit Insurance Organizations

CUDGC (AB) - http://www.cudgc.ab.ca

CUDGC (SK) - https://www.cudgc.sk.ca/about-us/

DGCM (MB) - http://depositguarantee.mb.ca/home/

DICO (ON) - http://www.dico.com/design/0_0_Eng.html

CDIC - https://www.cdic.ca

NCUA - https://www.ncua.gov

B.C. Ministry of Finance

FIA/CUIA Consultations - http://www.fin.gov.bc.ca/pld/fiareview.htm

FIA/CUIA Consultations Stakeholder Summary - http://www.fin.gov.bc.ca/pld/files/Response%20report%20to%20FIA%20review%20initial%20consultation%20paper.pdf

FIA/CUIA System Response - http://www.fin.gov.bc.ca/pld/files/BC%20Credit%20Union%20System%20Response.pdf

FIA/CUIA Response of Community Savings Credit Union - http://www.fin.gov.bc.ca/pld/files/Community%20Savings%20Credit%20Union%20(CSCU).pdf

BC Select Standing Committee on Public Accounts - Draft minutes, October 2016 - https://www.leg.bc.ca/documents-data/committees-transcripts/20161005am-PublicAccounts-Vancouver-Blues

Other References

Coast Capital Savings CU: CUDIC vs CDIC deposit insurance coverage - Report: https://www.coastcapitalsavings.com/SharedContent/documents/OnlineVoting/2016/ContinuanceBooklet.pdf

C.D. Howe Institute, ‘A New (Old) Way of Thinking about Financial Regulation’ (2014) - Report: https://www.cdhowe.org/sites/default/files/attachments/research_papers/mixed/Commentary_401_0.pdf

FDIC: Termination of unlimited deposit insurance - https://www.fdic.gov/news/news/financial/2012/fil12045.html

FSB: Guidance for Developing Effective Deposit Insurance Systems - http://www.fsb.org/wp-content/uploads/r_0109b.pdf

Time: Why ... a Huge Decline in Drivers Licenses - http://time.com/money/4185441/millennials-drivers-licenses-gen-x/

OECD: ‘Financial Turbulence - Some Lessons Regarding Deposit Insurance’ (2008) - Report: http://www.oecd.org/pensions/insurance/41420525.pdf

CATO: ‘The Explicit Cost of Government Deposit Insurance’ (2014) - Report: https://object.cato.org/sites/cato.org/files/serials/files/cato-journal/2014/2/v34n1-8.pdf

FDIC: ‘Deposit Insurance Reform: State of Debate’ (1999) - Report: https://www.fdic.gov/bank/analytical/banking/1999dec/1_v12n3.pdf

CCUA: 2015 Annual Report - https://www.ccua.com/~/media/CCUA/member_corner/publications/pdfs/CanadianCentral_AnnualReport_2015.pdf

World Bank: ‘Deposit Insurance Around The World - Issues of Design and Implementation’ (2008) - Report: https://mitpress.mit.edu/sites/default/files/titles/content/9780262042543_sch_0001.pdf

NBER: ‘Deposit Insurance Around the Globe’ (2001) - Report: http://www.nber.org/papers/w8493.pdf

Book: ‘Stress Tests: Reflections on Financial Crises’ (2014) - Book: https://www.amazon.ca/Stress-Test-Reflections-Financial-Crises/dp/0804138591

ACKNOWLEDGEMENT

The author wishes to thank selected credit union system veterans that generously volunteered technical expertise, system memory and professional guidance. Out of discretion then no names are noted. Thank you. Their wisdom, perspective and encouragement were most appreciated.

DISCLAIMER & COPYRIGHT

This article reflects the personal comments of the author, Ross McDonald. This article does not represent the views of any financial cooperative, corporate organization, regulatory body or government ministry. Comments are wholly based on information that is in the public domain.

Although the author has made every effort to ensure that the information in this article was correct at press time, the author does not assume and hereby disclaim any liability to any party for any loss, damage, or disruption caused by errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

All rights reserved.

Credit Union Deposit Insurance Policy - 1/2 - Overview, History, Pros & Cons

A policy of unlimited deposit insurance may have significantly supported system growth and membership confidence. But it is unknown outside of Western Canada, may cause moral hazard, and may be increasingly expensive to credit unions in terms of earnings, capital and compliance.

“A policy of unlimited deposit insurance may have significantly supported system growth and membership confidence. But it is unknown outside of Western Canada, may cause moral hazard, and may be increasingly expensive to credit unions in terms of earnings, capital and compliance.”

SERIES OVERVIEW

This article is the first part of a two-part series related to deposit insurance applicable to Canadian credit unions.

Overview, History & Pros/Cons: Policy in B.C. & Canada. Unlimited vs limited

Implications & Options: Benefits, cost & regulatory impact. Three policy choices